What Are Loss Run Reports: A Guide to Better Business Insurance Management

Introduction to Loss Run Reports

Think of loss run reports as the report card of your insurance history, detailing your claims, losses, and how they were settled.

Having a clear understanding of loss run reports can lead to better-informed decisions about your insurance needs, potentially saving your business money and headaches in the long run.

If you are shopping for a new insurance policy, you will need to get a loss run report from your current carrier to give to the agent. This is required by all carriers in order to provide a quote.

You can request a loss run report directly from your carrier. Many times you can do this through logging into the carriers portal and requesting it online.

What Loss Run Reports are Used For

Underwriting and Risk Assessment

🔍 Loss run reports, generated by insurance companies, provide detailed claim histories for various policy types over a specific time period, enabling underwriters to assess claim frequency and severity and determine potential premium impacts.

📊 Underwriters typically request loss runs covering 3-5 years in a hard market and 3-7 years in a soft market to evaluate a policyholder's claim activity history and identify any patterns or trends.

Claims Development and Impact

📈 Loss runs may reveal claims that developed over time, showing increases in payouts or defense costs, as well as the status change from open to closed claims, which can affect claim finalization and premium calculations.

Renewal and Reporting Practices

🔄 Insurance companies generally request loss runs annually during policy renewal or to review a policyholder's current claims history, even if reports were previously provided, as claims may be submitted after the policy period ends.

Accessibility and Ordering

📋 Loss run reports can be obtained from the insurance company, the producer or agency of record, or through specialized software programs that allow new agencies to access loss runs for policyholders they weren't previously associated with.

Components of a Loss Run Report

To effectively utilize loss run reports, it's essential to understand their components. Typically, a loss run report includes several key elements that provide a comprehensive overview of a business's claims history. First, you'll find detailed information about each claim, such as the date of the incident, the nature of the claim, and the amount paid out.

Moreover, loss run reports often categorize claims by type, which can help businesses identify trends or recurring issues. Another critical component is the reserve amounts, which represent the estimated future payout for ongoing claims. This information is crucial for businesses to gauge potential financial liabilities accurately.

By examining these components, businesses can gain a better understanding of their insurance profile and identify areas that need attention. This knowledge can be invaluable for refining risk management strategies and making more informed decisions about insurance coverage.

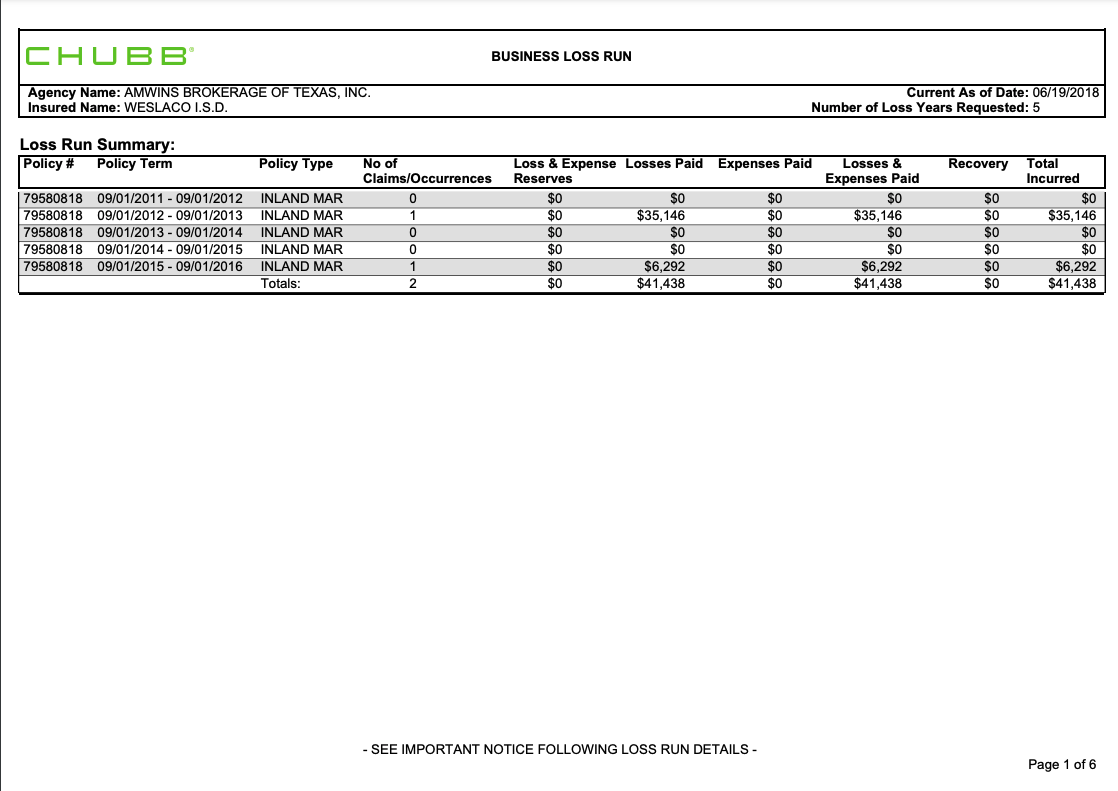

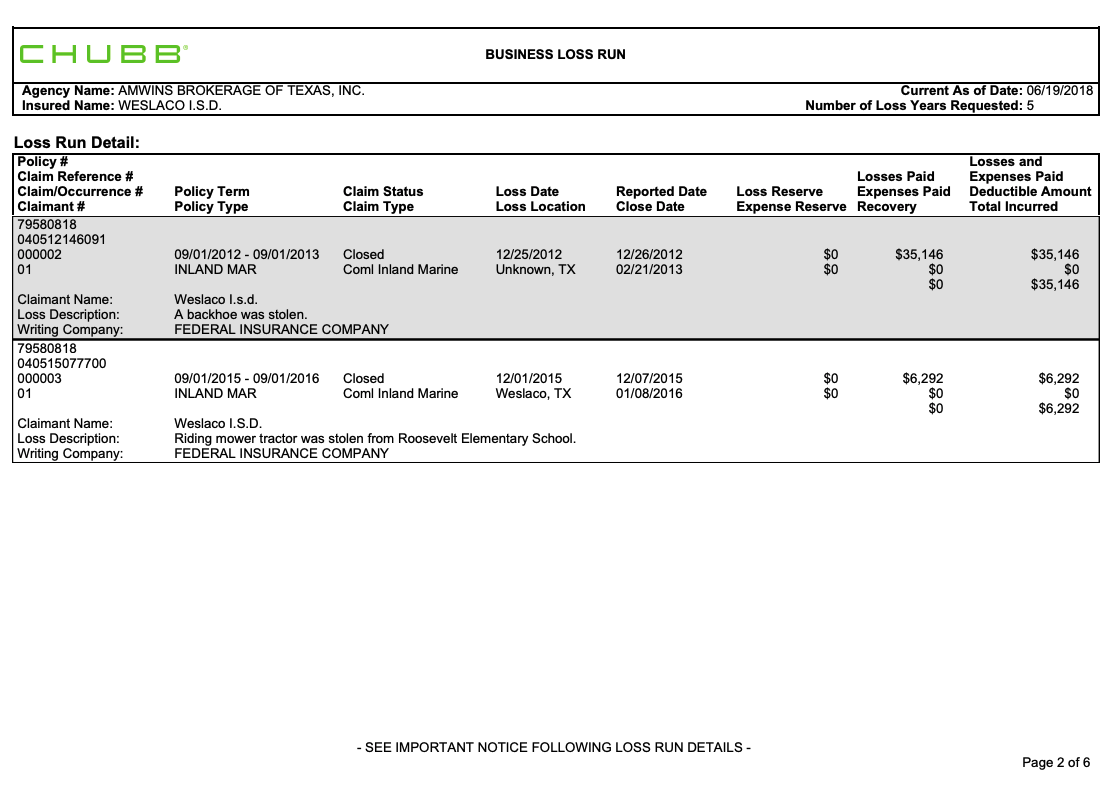

Sample Loss Run

Fast, Easy Life Insurance for Busy New Dads

How to Get Quality Chiropractic Liability Insurance Fast

Coterie Insurance and BTIS Carrier Comparison